S-Invest

Your investment funds savings plan in lux|funds.

"It’s a fact that most of our customers open a savings account for their children at birth. And being a young father myself, I perfectly understand that this is very convenient to do so, in order to permit family and friends to easily put some money on it at any occasion. The first months with a baby are indeed not the best ones to think about finance. However, let me explain why they are actually the right ones to choose an alternative, smarter way of saving money."

Take it into account to protect your children’s future

To save properly, it's essential to take inflation into account. Remember: what could you buy with EUR 20 in 2002, when the euro was introduced? Today, that same banknote has lost value. Here's why: prices have risen sharply for a large number of goods and products.

Inflation has been particularly marked in recent years, with a rate of 6,3 % in 2022 and 3,7 % in 2023.

Rather than focusing only on the amount of money you will put aside for your child, ask yourself what they will actually be able to buy with that money in a few years' time. With this in mind, you'll be able to better protect their savings against the loss of value due to inflation.

If you have 2,32%* interest on your child’s savings account and inflation is 3,70%**, you will definitely see a loss in purchasing power over the years, when you think you are actually “saving” money.

Luc Sinner - Deputy Head of Marketing

*Average interest rate for 2023 on the Tweenz savings account (0-12 years) for savings less than or equal to EUR 100.000

**Average inflation rate for 2023 – source: STATEC: Inflation - Statistics Portal - Luxembourg

This negative difference of 1,38% between the interest rate and inflation gradually erodes the real value of your savings.

In such a scenario, the EUR 10.000 you have today in your savings account will only be worth EUR 8.719 in about ten years. Given this significant loss of value (i.e. EUR -1.281), it is worth searching for better-performing alternatives to preserve and grow the wealth of your children.

Understand market dynamics using benchmark indicators

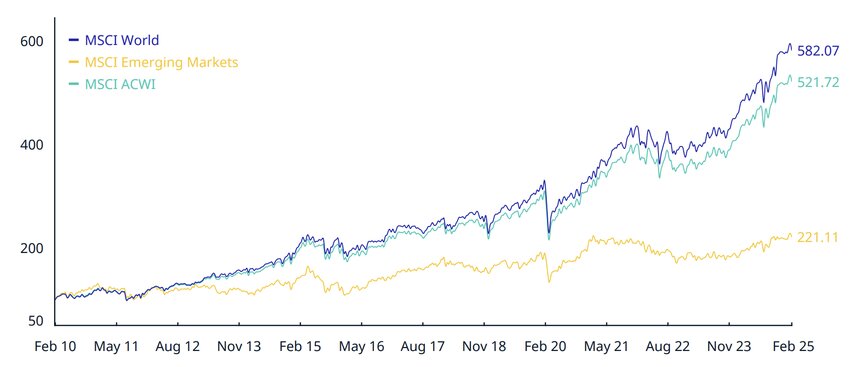

Historically, the global stock market has shown a long-term growth trend, despite short-term ups and downs. The MSCI World index represents an important benchmark as a starting point for investment.

In finance, an index is used to understand how the stock market is performing. The MSCI World is a global index that captures the performance of 1.500 companies (large and medium-sized), spread over 23 developed markets worldwide, including North America and the US, Europe, Asia and Australia.

Source: MSCI World Index

Make it a valuable asset for smart investing

We often say that children grow up fast. However, as a parent, you actually have more than 10 to 20 years to save for them - a valuable and often underestimated period to invest intelligently.

This long-term savings horizon provides an ideal framework for building a coherent investment strategy capable of generating solid returns.

Why take this into consideration? Because by combining regular investments with a long-term vision, you create the ideal conditions for benefiting from the growth of the financial markets. The MSCI World index has posted an average annual return of around 8% over more than 10 years - despite occasional economic crises.

Our advisors are here to help you define your investor profile and guide you towards the solutions best suited to your objectives.

Are you able to put aside a little money at the end of each month? Have you ever asked yourself how you could put that extra money to work, to increase its value rather than let it sit dormant in your savings account? We have the solution for you: Invest your money. Get started by opening your own securities portfolio.

![[Translate to English:]](/fileadmin/_processed_/8/f/csm_218__STI__ouvrir_et_gerer_un_portefeuille-titres_142cd029f7.jpg "[Translate to English:]")

Invoice fraud is now one of the most widespread and costly threats to businesses, regardless of their size or industry. It primarily targets business-to-business (B2B) payments and exploits a key factor: the trust established with your regular partners. Understanding how it works and developing the right reflexes is essential to avoid financial losses that are often irreversible. In this article, discover what you need to know about the topic.

![[Translate to English:]](/fileadmin/_processed_/c/1/csm_452_FIN_fraude_facture_17juin26_b4395d5ac3.jpg "[Translate to English:]")

Starting a career in Luxembourg often goes hand in hand with a first well-paid job, financial independence, and new life plans. However, one question frequently comes up among young professionals: “Do I really need to file a tax return if it isn’t mandatory?” The answer is simple: in most cases, yes — because it often is financially beneficial. Find out why in this article.

![[Translate to English:]](/fileadmin/_processed_/f/f/csm_451_FIN_jeunes_actifs_declaration_impots_2_e29be3eb82.jpg "[Translate to English:]")

On the occasion of E-Drive Day, cars no longer simply inspire dreams—they also reflect the major transformations of our time. Between rising oil prices, an accelerated energy transition, and new driver expectations, the automotive market is rapidly evolving . And the figures speak for themselves: electric vehicles are now emerging as an increasingly obvious choice, particularly through leasing options.

![[Translate to English:]](/fileadmin/_processed_/9/b/csm_450_FIN_mobilite_change_de_vitesse_a51518e4a7.jpg "[Translate to English:]")

Are you among the majority of taxpayers who file their tax returns in December? What if we tell you it isn’t a good idea? To start filling in your tax return at the beginning of the year is much better, and in this article we explain why.

![[Translate to English:]](/fileadmin/_processed_/4/f/csm_425_FIN_3_raisons_de_faire_sa_declaration_maintenant_3a63d0178a.png "[Translate to English:]")

Whether you manage your business alone or with a small team, financial tasks can be simplified or delegated thanks to a platform designed to make your day-to-day operations easier. Built to meet your professional needs, S-Net Business is continuously enhanced with new features. Discover how choosing S-Net Business can transform the way you work and help you boost your efficiency.

![[Translate to English:]](/fileadmin/_processed_/3/7/csm_448_FIN_Fonctionnalites_S-Net_Business_A_0eb4ec356a.jpg "[Translate to English:]")

Why Sophie should start her retirement planning today: The workday is over. Sophie is sitting in her living room, laptop closed, tasks completed. Her daughter Lily is already asleep and her husband Marc is at basketball practice. For the first time in a long while, Sophie can enjoy a moment just for herself. She picks up her smartphone and scrolls through the news. Suddenly, a headline catches her eye: “In 2026, contribute more to your retirement plan and enjoy tax benefits in 2027!” Sophie frowns. What does that mean for me? She has often thought about securing her future but kept postponing the decision. One thing is clear: when she retires, Sophie wants a life free of stress and full of comfort.

![[Translate to English:]](/fileadmin/_processed_/4/9/csm_443_Marc_et_Sophie_S-Pension_8eb784f1c7.jpg "[Translate to English:]")

Sophie and Marc had been talking about it for months. Between two coffees and a few scrolls through their favourite property app, they dreamed of a light-filled living room, a kitchen where Marc could finally test his recipes without bumping into the fridge… and a balcony for Sophie – because plants are simply a must.

![[Translate to English:]](/fileadmin/_processed_/3/2/csm_446_S_M_Le_grand_saut_vers_le_premier_logement_7116ee6967.jpg "[Translate to English:]")

In a context where rents are rising and interest rates are evolving, becoming a homeowner can offer much more than just a roof over your head. It’s a strategic choice—both personal and financial. In this article, we present the main advantages of buying real estate in both the short and long term, while also exploring the reasons why renting can make sense and when it might be the right time to take the step toward homeownership. Discover why buying a property can be a smart decision for your financial and personal future!

![[Translate to English:]](/fileadmin/_processed_/7/b/csm_444_FIN_Acheter_ou_louer_avantages_logement_46b7cb8e32.jpg "[Translate to English:]")

Your child is about to turn 18 - it’s hard to believe he is an adult now! It seems like just yesterday that you held him in your arms for the first time. That was, however, already 18 years ago. Time really does fly! The only thing that matters for him right now is to pass his driving licence and buy his first car.

Halfway through our careers, we look back and wonder why we didn’t think about the future sooner. Did you know that even as a non-resident, you can take out a supplementary pension, with all its benefits? Why is the S-Pension private pension scheme the right choice at this stage in your life?

![[Translate to English:]](/fileadmin/_processed_/6/c/csm_367_FIN_S-Pension_non_residents__1__7ed60e51c2.jpg "[Translate to English:]")

Do you have some savings tucked away? Or have you inherited some money? Sure, you could organise an awesome trip halfway around the world, make some luxury shopping, or simply put the money away in your savings account, however you do have other options to put your savings to work for you by carefully investing it. For beginners investors: in this article we present three approaches for you to flawlessly invest your savings.