Saving and investing

Generalities

-

Fonds de garantie des dépôts Luxembourg (FGDL) : your deposit guarantee scheme

Your deposit is covered by a contractual scheme officially recognised as a Deposit Guarantee Scheme. If insolvency of your credit institution should occur, your deposits will be repaid up to EUR 100,000.

Overall limit of protection

If a deposit is unavailable because a credit institution is unable to meet its financial obligations, depositors are repaid by a Deposit Guarantee Scheme. This repayment covers at maximum EUR 100,000 per credit institution. This means that all deposits at the same credit institution are added up in order to determine the coverage level. If, for instance a depositor holds a savings account with EUR 90,000 and a current account with EUR 20,000, he or she will only be repaid EUR 100,000.

The protection of deposits resulting from real estate transactions relating to private residential properties, as well as compensation received for losses incurred in connection with private residential property, deposits that serve social purposes and which are linked to particular life events of a depositor, such as marriage, divorce, retirement, dismissal, redundancy, invalidity or death and deposits that are based on the payment of insurance benefits or compensation awarded to victims of criminal offences

or wrongful conviction may exceed an amount equivalent to EUR 100,000, nevertheless without exceeding an amount equivalent to EUR 2,500,000, during 12 months after the amount has been credited or from the time these deposits can be legally transferred.

Further information can be obtained under www.fgdl.lu.

Limit of protection for joint accounts

In case of joint accounts, the limit of EUR 100,000 applies to each depositor.

However, deposits in an account to which two or more persons are entitled as partner of a company, member of an association or grouping of a similar nature, without legal personality, are aggregated and treated as if made by a single depositor for the purpose of calculating the limit of EUR 100,000.

Reimbursement

The responsible Deposit Guarantee Scheme is the "Fonds de garantie des dépôts Luxembourg" (FGDL), 283 route d’Arlon, L-1150 Luxembourg, (+352) 26 25 1-1, info@fgdl.lu, www.fgdl.lu. It will repay your deposits (up to EUR 100,000) within 7 working days.

If you have not been repaid within these deadlines, you should contact the Deposit Guarantee Scheme since the time to claim reimbursement may be barred after a certain time limit. Further information can be obtained under www.fgdl.lu.

Investor Protection Summary

The Luxembourg investor compensation scheme (SIIL) covers investors, physical persons and legal entities within the limits and according to the terms and conditions provided for by the law of 18 December 2015 relating to the resolution, recovery and liquidation measures of credit institutions and some investment firms, including deposit guarantee and investor compensation schemes.

The SIIL provides cover for claims resulting from a credit institution’s inability to:

- reimburse its investors the funds due to them or belonging to them, held on their behalf and related to investment transactions, in accordance with applicable legal and contractual conditions;

- or return to investors the instruments belonging to them and held by them, administered or managed on their behalf and related to investment transactions, in accordance with applicable legal and contractual conditions.

Investment transactions made by the same investor are covered up to an amount equivalent to EUR 20 000, whatever their currency or location within the European Union and regardless of the number of accounts held.

In case of an investment transaction involving a joint account, the claims are distributed evenly among the investors, if no special provisions have been provided.

Investors must be compensated as soon as possible by the SIIL, and this within three months at the latest.

-

The blocked savings account is a savings account that is frozen until the holder turns 18, enabling you to easily build up capital for youngsters entering adult life.

The account may be opened by a legal representative or a third party (grandparents, aunt, uncle, neighbour, etc.).

The person who opens the account is called the “depositor”.

-

The Tweenz and Axxess sight deposit accounts are intended for customers who, at any time, wish to save on their own behalf and have their funds at disposal. They have access to these funds starting from their 15th birthday.

A blocked savings account is frozen until they turn 18, but offers the best interest rate among all of Spuerkeess's sight deposit accounts for young people.

-

Unlike a traditional savings account, BHW offers a guaranteed interest rate and the possibility of deducting the amount saved from your taxable income (within the legally established limit). The BHW contract also makes it easier for you to buy your first home with public assistance, such as the State Guarantee.

-

If you are experiencing financial difficulties, you can suspend payments to your BHW account and resume making payments at any time. However, if you are saving with the goal of receiving the State Guarantee, it is recommended that you contact a Spuerkeess advisor before suspending payments to preserve your eligibility.

-

You can withdraw funds from your housing savings scheme account if necessary, provided that the funds are ultimately invested in your main residence. 'Investment' is understood to mean: buying, building or renovating an apartment/home; buying land on which to build an apartment/home; or repaying the real estate loan on your main residence. Before taking any action, Spuerkeess recommends that you contact the Luxembourg Direct Contributions Administration or a BHW advisor by calling 44 88 44 – 1.

-

It is a life insurance product destined to finance children’s studies.

LALUX Study Cover enables parents or any other person with a link to a child (e.g. godparents, grandparents) to build up long-term savings for that child, which will be made available to them in the form of quarterly payments, once they begin their studies or start work.

The minimum contract duration is ten years, and the contract must be concluded before the child’s 12th birthday.

-

If the policyholder dies during the life of the contract, then the insurance is typically continued, since the premium is paid by lalux. The capital therefore remains guaranteed at maturity.

Exception: If the policyholder dies in the first 5 years, the contract is terminated, and the premiums paid by the deceased up to that point are refunded.

-

The first "10” represents the capital in the event of death, and the second "10” the capital in the event of survival. Thus, with a 10/10 policy, at the end of the contract, the policyholder shall have as much capital as his beneficiaries would have had in the event of his death before the end of the contract.

Please note: If the policyholder dies in the first 5 years, death benefits are limited to the sum of the premiums paid until then.

-

- To open a Speedinvest, the initial minimum investment is EUR 500.

- You may also establish a standing order in favour of your Speedinvest. Nonetheless, the minimum amount of your standing order may not be less than EUR 50.

- The minimum amount of additional investments, and respectively disinvestments, is set at EUR 50.

- Any disinvestment bringing the balance of your Speedinvest below EUR 500, will require the closure of your Speedinvest.

-

Speedinvest is a product with no transaction fees, custody fees, or closing charges.

A management fee of 0,25% per year (excluding VAT) will be withdrawn quarterly. It is applied to the average of your Speedinvest assets for the past quarter.

The charges related to financial instruments (the charges that are withdrawn by the fund over a year) amount to approximately 1%.

-

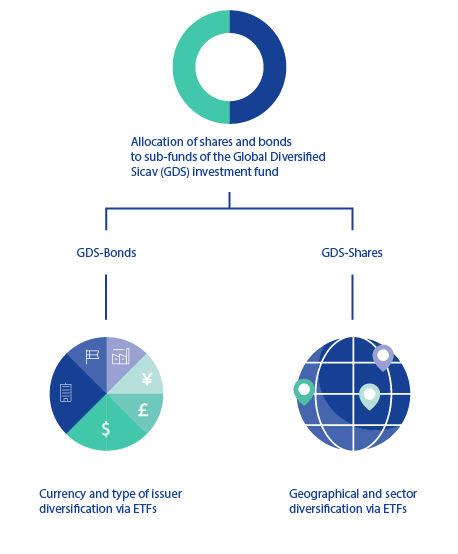

In accordance with the chosen strategy, your money will be invested in two Global Diversified Sicav (GDS) subfunds - a bond subfund and an equity subfund – that are mainly composed of Exchange-Traded Funds (ETFs). They were specially created for Speedinvest. he ETFs take a diversified approach when investing in international stock markets and in bonds denominated in EUR and USD.

-

S-Invest is Spuerkeess's savings plan that invests your savings in SICAV funds. It functions as a standing payment order from your checking account to your securities account. You can change the frequency and amount of your S-Invest plan at any time, as with all standing orders. What's more, our S-Net web banking solution allows you to easily sign up for and manage your S-Invest plan from the comfort of your own home.

-

Your choice will mainly depend on your investment horizon and risk tolerance.

The guidance below does not constitute investment advice.

SubfundsMaximum capital invested in equitiesRisk profileInvestment horizonLUX-PENSION 100%100% equities. For investors seeking maximum performance potential and willing to accept the associated risks.AggressiveLongLUX-PENSION 75%75% equities, 25% bonds. For investors who accept fluctuations in exchange for high performance potential.AggressiveLongLUX-PENSION 50%50% equities, 50% bonds. For investors seeking a balance between security and return.ModerateMedium to longLUX-PENSION 25%25% equities, 75% bonds. For investors seeking some growth potential while remaining cautious.CautiousShort to mediumLUX-PENSION MARCHE MONETAIRE0 % equities, 100% bonds. For cautious investors who prioritise security and are willing to accept a limited return.CautiousShort -

When the contract matures, you will receive full repayment of the accumulated capital, plus any returns. This capital repayment under the S-Pension contract is subject to taxation at half the overall rate. For most customers, it is recommended to defer repayment until retirement, as their tax rate will then be lower than at the end of their career.

-

- One-off transfers: you make transfers whenever you want, with no commitment to a specific frequency. You can fund your contract according to your financial availability or your plans.

- Regular transfers: you choose a fixed frequency (monthly, quarterly, half-yearly or annually) and set up automatic transfers to fund your contract.

-

You can terminate your S-Pension contract via S-Net mail.

Early repayment of your S-Pension, before the minimum subscription period of 10 years or before the age of 60, is in general excluded and subject to tax penalties (except in the event of death, invalidity or serious illness).

The tax authorities (Administration des Contributions Directes) will tax the total amount repaid in full at the standard rate (according to the tax scale) together with other income for the year of taxation. Early redemption therefore does not involve retroactive taxation of the tax advantage, but taxation as net miscellaneous income for the year in which the redemption takes place.

Partial repayment is not possible.

If you have never taken advantage of the tax benefits associated with S-Pension, you can close your S-Pension plan without incurring any tax penalties.

Please let us know how you wish to proceed.

-

When you approve an order via S-Net, your instructions are definitively submitted to Spuerkeess. Please note that orders, once submitted, are irrevocable and therefore cannot be cancelled.

The stock exchange order book associated with your S-Net agreement displays all transactions carried out via S-net during the preceding 12-month period, as well as all transactions carried out via other distribution channels.

By default, the order book includes all pending orders for all securities accounts associated with the agreement. You can check the status and progress of all orders as they change status from "preparing order" to "complete", allowing you to keep tabs on the order as it is processed.

If an order is rejected, a secure message indicating the reason for the rejection will be sent to you via the S-Net messaging service as soon as possible.

-

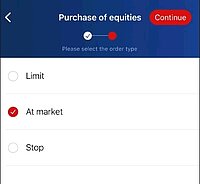

“Stop” orders can be made via S-net for the following stock exchanges: Amsterdam, Brussels, Lisbon, Paris, Berlin, Düsseldorf, Frankfurt, Hamburg, Munich, Stuttgart, Xetra, Vienna, NYSE & AMEX.

It is an order to sell or buy equities that is activated when the share price reaches a specified value, known as the “Stop” price. The “Stop” price activates the “Stop” order. At that point, it becomes an “At Market” order and is filled at the next possible price, which may be above or below the “Stop” price.

Securities portfolio

-

A securities portfolio is an investment account used to hold and manage financial instruments: equities, bonds, ETFs, investment funds, precious metals, etc...

It allows you to invest freely in the financial markets and thus diversify your savings. The risk associated with the securities portfolio depends on the financial instruments in which you have invested.

For more information, please refer to “A guide for investors” available at www.spuerkeess.lu.

-

The money invested in your securities portfolio is not locked and you can sell your financial instruments at any time via your online banking S-Net or your branch advisor. However, the counter-value of the financial instruments may have fallen at the time of the sale. Moreover, capital gains realised on shareholdings held for less than six months are subject to income tax in Luxembourg.

For more information, please refer to “A guide for investors” available at www.spuerkeess.lu.

-

If you buy or sell a security in a currency other than that of your current account (for example: a security priced in USD if your current account is denominated in EUR), an exchange fee of 0,10%, with a minimum of EUR 2,50 and a maximum of EUR 125, will be applied. To limit the impact of this fee when investing on the stock market, you can open a foreign currency account via the Store of your S-Net online banking. In this case, the exchange fee will only be applied when you transfer money from your foreign currency account to your current account in euros and not on each purchase/sale of securities.

-

The taxation applicable to securities portfolios in Luxembourg is relatively favourable, particularly for retail investors, but it varies according to the type of income generated (capital gains, dividends, interest) and the length of time the securities are held.

1. Capital gains tax on securities

- If the securities are held for more than 6 months and do not represent a significant shareholding (<10% of the company's share capital), capital gains are not taxable.

- If the shareholding is significant (>10% of the company’s share capital), capital gains are subject to income tax.

2. Dividends

- Dividends are generally subject to a 15% withholding tax.

3. Interest

- Interest received is generally subject to a 20% withholding tax.