An April without a weak spot

Investment Update - May 2026

April was an exceptional month for the financial markets, with global indices rebounding by +7,9%*. This followed a decline of almost 5%* in March and pushed global markets back to record highs.

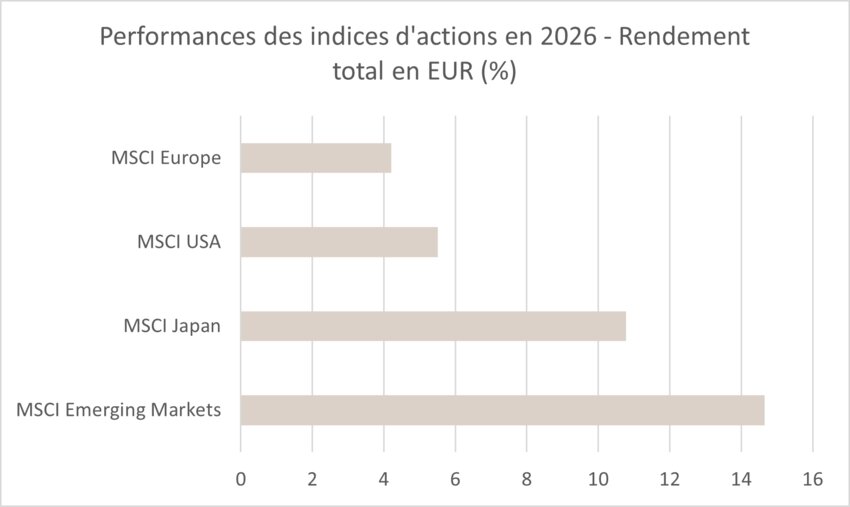

The rebound was driven chiefly by the US market (+8,6%*), with Technology stocks at the forefront (+15%). Emerging markets, which remain particularly sensitive to developments in the conflict with Iran, also posted a solid performance of +12,9%*. Europe, where the strength of the economic recovery remains uncertain, lagged behind somewhat, rising by a more modest +5,4%*.

In March, investors had significantly reduced their equity exposure, paving the way for April’s sharp rebound as positions were quickly rebuilt. At the same time, earnings expectations continue to improve, supported in particular by the still-strong investment cycle linked to artificial intelligence (AI).

Two key drivers are still underpinning the US economy: investment in AI and resilient household spending, buoyed by tax credits. While higher energy prices are weighing on disposable income, these tax incentives are largely offsetting the pressure, as several studies have shown.

The energy shock is reigniting inflationary pressure. Inflation could therefore move back towards 3% during 2026, both in Europe and in the United States.

Europe, which is considerably more sensitive than the United States to energy costs, is coming under greater strain. Even Germany’s investment programme, which was expected to support growth, appears to be progressing more slowly than initially hoped.

This divergence is shaping very different expectations for monetary policy on either side of the Atlantic. While investors broadly believe that the US Federal Reserve (Fed) can afford to keep rates unchanged for the time being, expectations are building around the possibility of the European Central Bank (ECB) raising key interest rates.

Against a macroeconomic backdrop that remains relatively stable in the United States, corporate earnings continue to support the strong market rally.

In this environment, asset allocation remains clearly tilted towards risk assets, with equities favoured over bonds. From a geographical standpoint, preference is still given to the United States and emerging markets, where growth prospects appear stronger at both macroeconomic and company level than in Europe. In sectoral terms, the AI theme remains dominant, particularly through Technology and Communication Services. In fixed income, corporate bonds are preferred to government debt in order to capture the more attractive yields available following the market stress caused by the Middle East conflict.

*Performances are calculated in euros.

Stock markets

April saw an especially strong rebound in equity markets despite continued geopolitical uncertainty. The MSCI World gained +7,9%*, driven mainly by emerging markets (+12,9%*), North America (+8,6%*) and Europe to a lesser extent (+5,4%). In the US, both the S&P 500 and the Nasdaq reached record highs, supported by robust corporate earnings and expectations of substantial AI-related investment.

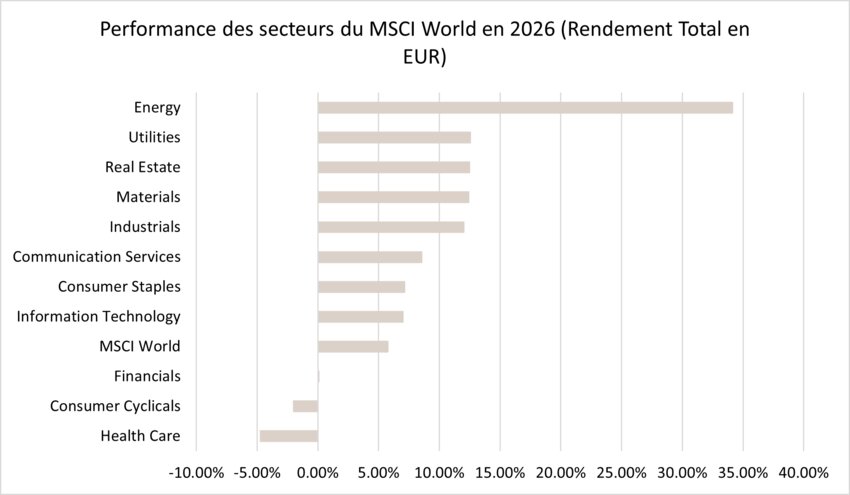

Performance varied significantly across sectors. In Europe, Technology, Banks and Financial Services led the advance amid rising long-term yields, while Healthcare and more defensive sectors lagged behind. In the US, market leadership remained concentrated in growth stocks, notably Communication Services and Technology. Meanwhile, the Energy sector declined over the month despite oil prices remaining above USD 100 per barrel, highlighting the gap between fundamentals and investor positioning.

Given the speed of the rally and the scale of investor repositioning, some tactical positions were scaled back. Long-term convictions nevertheless remain intact for Technology, Biotechnology and industrial companies benefiting from structural trends such as AI investment, reshoring and energy independence. In contrast, Consumer Discretionary was downgraded to neutral due to macroeconomic concerns and the combined impact of oil prices, inflation and interest rates. Energy and Utilities were also moved back to neutral as a hedging measure.

Market performance remains heavily concentrated in a limited number of sectors and stocks, a backdrop that has historically favoured sector rotation. Developments in the Middle East therefore remain critical: any easing of tensions could support a rebound in cyclical sectors, while a prolonged conflict would likely boost demand for defensive assets. In the event of a rapid de-escalation, emerging markets and cyclical stocks would appear best placed to benefit.

*Performances are calculated in euros

Sovereign yields and credit market

April extended the trend seen in March, with the conflict in the Middle East and disruption in the Strait of Hormuz continuing to dominate bond markets. Sovereign yields fluctuated sharply throughout the month as markets swung between hopes of de-escalation and fears of a prolonged conflict.

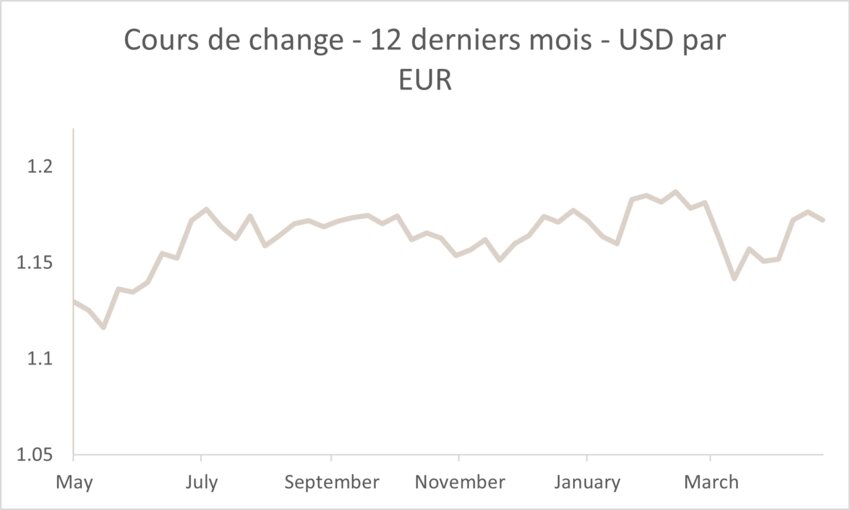

In the United States, yields initially reacted to developments surrounding Iran before moving higher in the second half of the month, driven by rising oil prices, relatively resilient economic data and a Federal Reserve perceived as less dovish. At its meeting at the end of April, the central bank left rates unchanged. However, internal divisions within the committee and Jerome Powell’s cautious tone led markets to scale back expectations for rate cuts this year. By month-end, the US 10-year Treasury yield had risen by 6 basis points (bps) to around 4,37%.

In the eurozone, bond markets proved even more sensitive to energy-related risks. Rising oil and gas prices fuelled inflation expectations and renewed speculation that the ECB could raise rates again. A brief ceasefire announced at the start of April temporarily eased pressure on yields, but the lack of any lasting agreement quickly reignited concerns. At the end of the month, the ECB kept rates unchanged while indicating that a June rate increase remained possible. The 10-year Bund thus ended April at 3,03%, up slightly compared to March.

Credit markets recovered strongly in April following the widening in spreads seen during March. In the eurozone, Investment Grade spreads narrowed by 15 bps to 80 bps, while High Yield tightened by 57 bps to 280 bps. The return of risk appetite following the ceasefire between the United States and Iran helped drive this recovery, triggering a rebound in the sectors hardest hit the previous month.

Disclaimer

The recommendations contained in this document are, unless otherwise expressly stated, those of Spuerkeess Asset Management and are produced by Carlo Stronck, Managing Director & Conducting Officer, Aykut Efe, Economist & Strategist, Guillaume Gehant, Portfolio Manager and Martin Gallienne, Portfolio Manager, acting under an employment contract with Spuerkeess Asset Management.

Spuerkeess Asset Management is an entity supervised by the CSSF (Luxembourg’s financial sector supervisory authority) as a UCITS management company able to provide discretionary portfolio management and investment advisory services.

All external sources (financial information systems, Bloomberg and Refinitiv Datastream) are, unless expressly stated in the recommendation itself, deemed reliable, it being understood that Spuerkeess Asset Management cannot, however, fully guarantee the accuracy, completeness or relevance of the information used by these sources. The information may be either incomplete or condensed and cannot be used as the sole basis for valuing securities.

The valuation of financial instruments and issuers contained in this document is based on data provided by Bloomberg. The full description of the valuation method used by Bloomberg is available at www.bloomberg.com.

Any reference to past performances should not be construed as an indication of future performances. The price or value of the investments to which this document refers directly or indirectly may vary at any time against your interests. Any investment in financial instruments entails certain risks of which Spuerkeess (Banque et Caisse d’Épargne de l’État, Luxembourg) has been informed beforehand, such as the loss of the investment made.

With a view to providing these recommendations to Spuerkeess, Spuerkeess Asset Management has verified all relationships and circumstances that could reasonably be likely to undermine the objectivity of the recommendations contained in this document and confirms the absence of interests and conflicts of interest relating to any financial instrument or issuer to which the recommendations relate directly or indirectly, as well as those of the persons involved in producing these recommendations.

Recommendations are made on the date indicated on the first page of the document and were first released on the same date. The recommendations contained in this document may, where applicable, be used and therefore updated when Spuerkeess Asset Management next provides investment advice to Spuerkeess.

All recommendations sent by Spuerkeess Asset Management to Spuerkeess over the past twelve months may be consulted directly and free of charge at Spuerkeess Asset Management’s registered office, 19-21 rue Goethe, L-1637 Luxembourg. The information to be consulted shall include the date of dissemination of the recommendation concerned, the identity of the individual(s) involved in the production of the recommendation, the target price and the relevant market price at the time of dissemination, the direction of the recommendation concerned and the period of validity of the target price or recommendation.

The information contained in this document cannot be used as the sole basis for valuing securities and this document does not constitute an issue prospectus.

This document is for information purposes only and does not constitute an offer or solicitation to buy, sell or subscribe. Spuerkeess Asset Management may not be held liable for any consequences that may result from the use of any of the opinions or information contained in this document. The same is true for any omissions.

Spuerkeess Asset Management does not accept any liability for this document if it has been altered, distorted or falsified, particularly through online use.