Markets buoyed by the merry month of May

Investment Update - June 2026

May was a record-breaking month for equity markets, with monthly performance reaching 5,7%*. This result is all the more remarkable given that it followed gains of more than 8%* in April.

Admittedly, the conflict with Iran has not been fully resolved. However, the ceasefire phases and the willingness of both parties to negotiate have been sufficient to prevent an uncontrolled surge in oil prices, the true arbiter of risk appetite in financial markets.

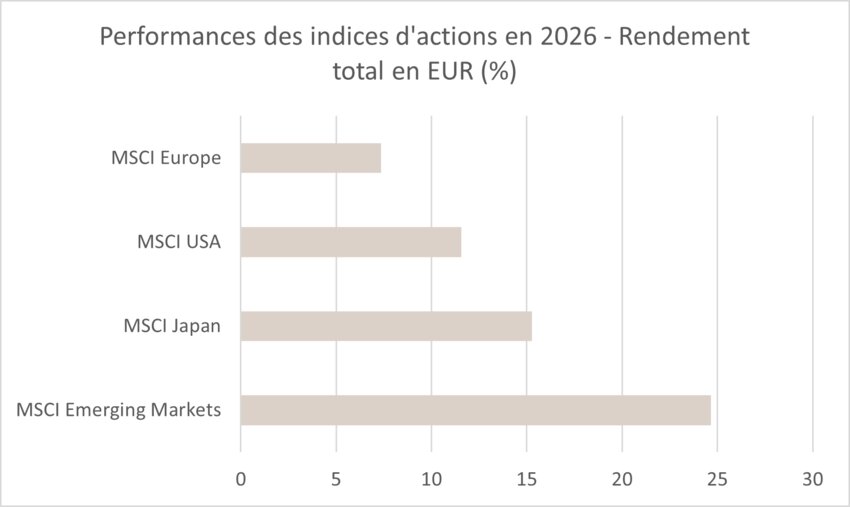

From a geographical perspective, emerging and US markets clearly outperformed, posting returns of 10%* and 5%* respectively, compared with a more modest 3,33%* for Europe.

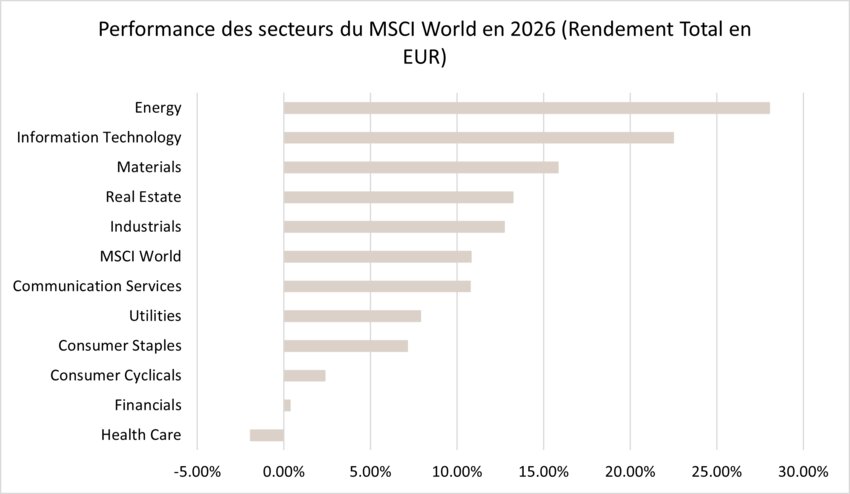

Yet these spectacular performances cannot be explained solely by the easing of concerns surrounding Iran. Indeed, the latest earnings season delivered exceptionally strong results overall, with technology companies reporting earnings that significantly exceeded expectations, driven by the surge in investment in artificial intelligence. It comes as no surprise that Technology, particularly the semiconductor subsector, was by far the best-performing sector in May. Given the strong momentum of semiconductors, it is no coincidence that emerging markets, where roughly half of market capitalisation is concentrated in three companies from this subsector, achieved such impressive returns.

On the economic front, the latest data confirm that inflation is returning and becoming increasingly embedded. Consumer prices are rising, as are the prices businesses pay to producers. In response, the European Central Bank (ECB) has signalled a forthcoming tightening of monetary policy, in line with market expectations. Its US counterpart, the Federal Reserve (Fed), maintained the status quo by removing the slight dovish bias that had appeared in its most recent communications.

Meanwhile, activity remains robust in the United States and fragile in Europe. US consumer spending remains resilient despite inflation, while investment in artificial intelligence continues to provide substantial support to growth. In Europe, the long-awaited recovery continues to disappoint, with growth forecasts in Germany being revised downwards once again.

Overall, interest rates have risen in response to the resurgence of inflation, fuelled both by substantial investment spending and movements in oil prices. US 10-year government bond yields ended the month at almost 4,50%, a symbolic threshold above which risk appetite tends to be affected, after approaching 4,70% during the month. The German 10-year yield returned to 3% after reaching 3,20% earlier in May.

From an allocation perspective, these exceptional gains achieved over a short period point in favour of profit-taking. This is particularly the case in emerging markets, which have become highly concentrated in a handful of semiconductor companies. As a result, exposure is being modestly increased to Europe, a region that investors have largely neglected in recent months.

Within fixed income, credit remains preferred to government bonds, which continue to face inflationary pressures and structural public deficit concerns. Similarly, duration is being kept relatively short across portfolios.

*Performances are calculated in euros.

Stock markets

May was marked by the continued rise in equity markets, despite elevated volatility linked to oil prices, interest rates and geopolitical tensions. Once again, the United States led the way: the S&P 500 reached new record highs while the Nasdaq delivered strong gains, supported by the ongoing strength of the artificial intelligence theme. Against this backdrop, the MSCI World advanced by 5,09%, driven by the US market (+5,56%), while the MSCI Europe was less dynamic, posting a more modest gain of +3,33%*. Emerging markets, benefiting from their increasing concentration around the AI theme, rose by +10,21% during the month.

After a strong start to the month, supported by an exceptionally solid earnings season, markets were temporarily unsettled by the rise in oil prices above USD 100 per barrel and inflation data that exceeded expectations. However, sentiment improved at the end of the month thanks to the decline in the geopolitical risk premium and the easing of long-term yields. Sector dispersion remained pronounced. Technology led performance thanks to record earnings, driven by semiconductors, data centre infrastructure and the memory segment, which has emerged as a new driver of the AI investment theme. Stocks exposed to the artificial intelligence value chain continued to benefit from upward earnings revisions, confirming both the depth of the investment cycle and the strong fundamental support underpinning this historic rally. By contrast, the Energy sector experienced a more mixed month. Initially supported by rising oil prices and the closure of the Strait of Hormuz, it subsequently underperformed as negotiations between the United States and Iran revived hopes of de-escalation. Interest rate-sensitive sectors, such as Real Estate and Utilities, remained under pressure due to bond market volatility.

Against this backdrop, long-term convictions remain focused on the AI theme generally, and on selected industrial companies linked to electrification and growing capacity requirements in particular. Nevertheless, it is important to monitor risks and take profits on certain positions, especially within the technology sector and emerging markets, both of which have become heavily concentrated around the same AI theme. At the same time, exposure to oilfield services companies has been increased in anticipation of investment requirements once the conflict with Iran is resolved. In addition, exposure to small and mid-cap companies has been established in order to benefit from the resilience of the US economy and the broadening of earnings growth across sectors.

*Performances are calculated in euros

Sovereign yields and credit market

May continued the trend established in March, with markets still dominated by developments in the Middle East conflict and uncertainty surrounding the Strait of Hormuz. Bond markets continued to fluctuate between inflation concerns linked to energy prices and hopes for diplomatic progress, reacting to developments in discussions between the United States and Iran. The oil market remained the primary transmission channel. The International Energy Agency highlighted that disruption to the Strait of Hormuz, a major shipping route, had placed significant pressure on global inventories. Crude oil prices fluctuated sharply before retreating towards the end of the month amid hopes of an agreement.

In the United States, persistent energy-related tensions and an ongoing restrictive interpretation of monetary policy initially pushed yields higher. Although the Fed did not meet in May, the publication on 20 May of the minutes from the 28-29 April meeting confirmed its cautious stance, its continued focus on inflation remaining above target, and its limited appetite for policy easing. Moreover, Kevin Warsh took office as Fed Chairman on 22 May, increasing market attention on the June meeting. Finally, the US 10-year ended May at around 4,45%, compared with 4,37% at the end of April, i.e. an increase of around 8 bp.

In the eurozone, bond markets remained highly sensitive to energy risk and monetary policy expectations. The ECB did not hold a meeting in May either, but the minutes of the April meeting, published on 28 May, showed that markets had already largely priced in an interest rate increase in June, against a backdrop of inflation fuelled by the oil shock. However, the easing of energy prices at the end of the month and hopes of an agreement between the United States and Iran led to an easing of long-term yields. As a result, the 10-year Bund ended May close to 2,97%, slightly below its level at the end of April.

In the credit space, markets continued to perform well in May, extending the recovery that followed the widening of spreads in March. In the eurozone, Investment Grade spreads remained relatively stable at around 80 bp, while High Yield spreads widened by around 7 bp to end the month at around 287 bp. In the United States, risk premiums fell slightly, supported by investors' search for carry and the resilience of corporate fundamentals.

Disclaimer

The recommendations contained in this document are, unless otherwise expressly stated, those of Spuerkeess Asset Management and are produced by Carlo Stronck, Managing Director & Conducting Officer, Aykut Efe, Economist & Strategist, Guillaume Gehant, Portfolio Manager and Martin Gallienne, Portfolio Manager, acting under an employment contract with Spuerkeess Asset Management.

Spuerkeess Asset Management is an entity supervised by the CSSF (Luxembourg’s financial sector supervisory authority) as a UCITS management company able to provide discretionary portfolio management and investment advisory services.

All external sources (financial information systems, Bloomberg and Refinitiv Datastream) are, unless expressly stated in the recommendation itself, deemed reliable, it being understood that Spuerkeess Asset Management cannot, however, fully guarantee the accuracy, completeness or relevance of the information used by these sources. The information may be either incomplete or condensed and cannot be used as the sole basis for valuing securities.

The valuation of financial instruments and issuers contained in this document is based on data provided by Bloomberg. The full description of the valuation method used by Bloomberg is available at www.bloomberg.com.

Any reference to past performances should not be construed as an indication of future performances. The price or value of the investments to which this document refers directly or indirectly may vary at any time against your interests. Any investment in financial instruments entails certain risks of which Spuerkeess (Banque et Caisse d’Épargne de l’État, Luxembourg) has been informed beforehand, such as the loss of the investment made.

With a view to providing these recommendations to Spuerkeess, Spuerkeess Asset Management has verified all relationships and circumstances that could reasonably be likely to undermine the objectivity of the recommendations contained in this document and confirms the absence of interests and conflicts of interest relating to any financial instrument or issuer to which the recommendations relate directly or indirectly, as well as those of the persons involved in producing these recommendations.

Recommendations are made on the date indicated on the first page of the document and were first released on the same date. The recommendations contained in this document may, where applicable, be used and therefore updated when Spuerkeess Asset Management next provides investment advice to Spuerkeess.

All recommendations sent by Spuerkeess Asset Management to Spuerkeess over the past twelve months may be consulted directly and free of charge at Spuerkeess Asset Management’s registered office, 19-21 rue Goethe, L-1637 Luxembourg. The information to be consulted shall include the date of dissemination of the recommendation concerned, the identity of the individual(s) involved in the production of the recommendation, the target price and the relevant market price at the time of dissemination, the direction of the recommendation concerned and the period of validity of the target price or recommendation.

The information contained in this document cannot be used as the sole basis for valuing securities and this document does not constitute an issue prospectus.

This document is for information purposes only and does not constitute an offer or solicitation to buy, sell or subscribe. Spuerkeess Asset Management may not be held liable for any consequences that may result from the use of any of the opinions or information contained in this document. The same is true for any omissions.

Spuerkeess Asset Management does not accept any liability for this document if it has been altered, distorted or falsified, particularly through online use.