A well-earned breather

Investment Update - July 2026

After two months of remarkable performance on equity markets, global indices posted more modest gains (+1,25%*).

Having benefited from a strong trend in Tech and AI on US and emerging markets between April and May, investors favoured the European markets: they posted a performance of 3,05%* at the end of June. Meanwhile, the US markets posted a performance of only 1,31%* and emerging markets were only marginally positive (+0,86%*).

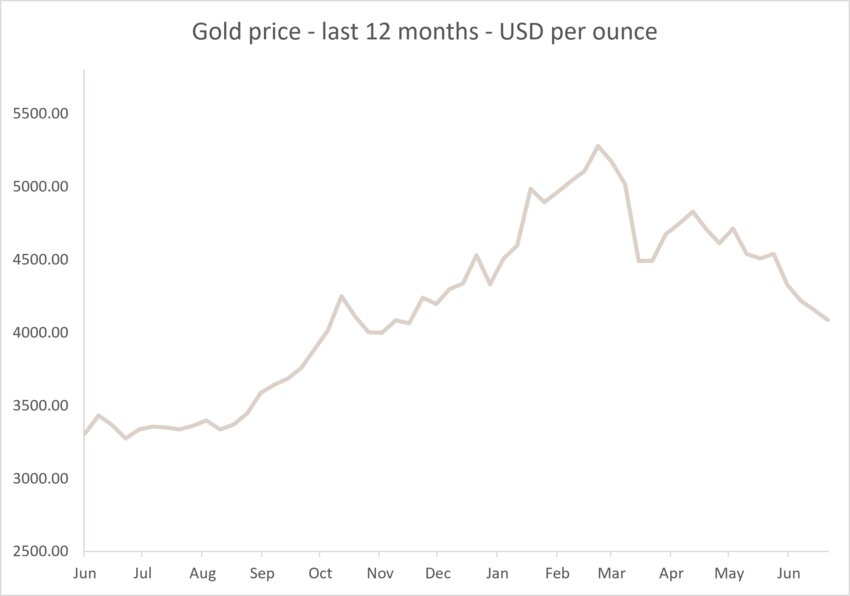

The easing of the conflict in Iran, along with the conflicting news surrounding hopes for a resolution, was likely one of the most favourable developments of the past month. The truce brought Brent crude down by 20%, ending the month at USD 72. As traffic through the Strait of Hormuz partially resumed, the premium on oil premium, compared with February's level, gradually unwound throughout June.

This easing of pressure on oil also relieved tension in the bond market, with sovereign yields edging slightly lower. After trading at 4,70% in May, the US 10-year yield closed just below 4,50%. Similarly, the German 10-year rate, which had reached 3,20% in May, ended June at 2,90%.

The European Central Bank (ECB) demonstrated its sensitivity to inflation and raised its key rates by 25 basis points. Its deposit rate now stands at 2,25%. It should be noted, however, that the recent easing in oil prices calls into question the need for a second rate hike, which is generally expected to follow the first. Indeed, preliminary June inflation figures are already showing an improvement: annual inflation came in at 2,8% (-0,4 percentage points versus May), with core inflation improving significantly to 2,4% from 2,6% in May.

In the United States, the change of leadership at the Federal Reserve (Fed) has brought its share of uncertainty. At his first FOMC meeting, new Chair Kevin Warsh was reserved, indicating that the Fed would communicate less about its future moves in an effort to “clean up” its relationship with the markets. The Fed will aim not only to be less voluble, but also to be slightly more hawkish on inflation, with Warsh expressing discomfort that inflation has remained above target for “too long”. Fortunately, the recent decline in inflation expectations has not led markets to price in an aggressive response, with only one rate hike expected in the coming months.

With fears of stagflation receding, the economic backdrop is improving. Thus, the overall allocation remains favourable to risk, with equities overweight at the expense of bonds. In June, the gradual fading of stagflation risks that had weighed on Europe triggered a rally in European equities, particularly in industrials and financials. On the other hand, emerging markets, overly concentrated in just three companies, were moved from overweight to neutral.

From a sector perspective, profit-taking on the AI theme led to a neutralisation of positions in Technology. In addition, cyclicality continues to be sought out via sectors such as Industrials and Banks. Finally, a preference for Biotechnology remains in place within the portfolios. Geographically, neutrality has been maintained across regions. Following the improvement in economic prospects in Europe, positioning on the region had already moved from underweight to neutral in May. In the United States, profit-taking following solid performances has moved positioning from overweight to neutral, in line with emerging markets, whose positioning had likewise been shifted to neutral.

On the fixed income side, duration remains contained, with a continued preference for credit over sovereign bonds.

*Performances are calculated in euros.

Stock markets

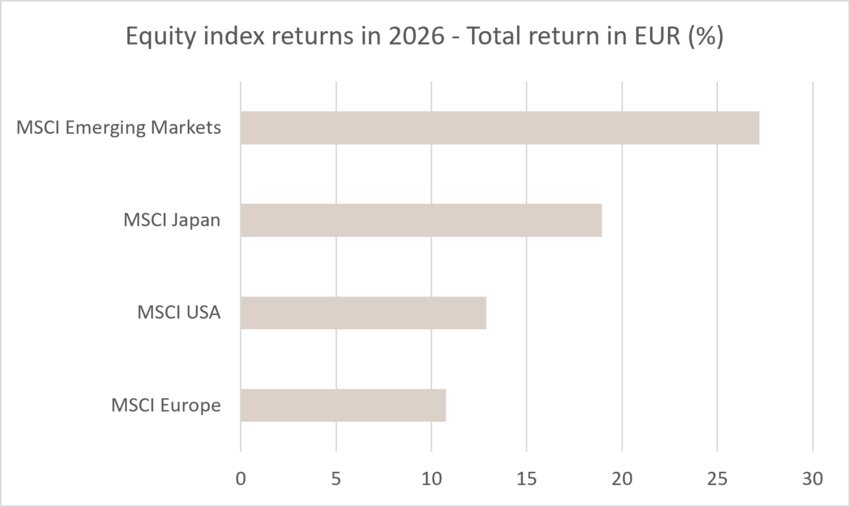

In June, equity markets continued to rise despite an uncertain geopolitical environment. The MSCI Europe posted the best performance among the major regions (+3,05%*), ahead of Japan (+1,87%*) and North America (+1,31%*), while emerging markets rose more modestly (+0,86%*). China was the exception: it lost 4,96%*, weighed down by persistent concerns over domestic demand.

Investors remained focused on developments in the Middle East conflict, with the signing of the memorandum of understanding between the United States and Iran fuelling hopes of a gradual reopening of the Strait of Hormuz. At the same time, central banks maintained a firm tone in the face of persistently high inflation, leading markets to anticipate more hawkish monetary tightening in both the United States and Europe. Despite this backdrop, CEOs at the annual leadership conference delivered a broadly reassuring message, highlighting continued robust demand in the United States, a strong ability to pass on inflation through prices, and sustained investment in artificial intelligence and data centre infrastructure.

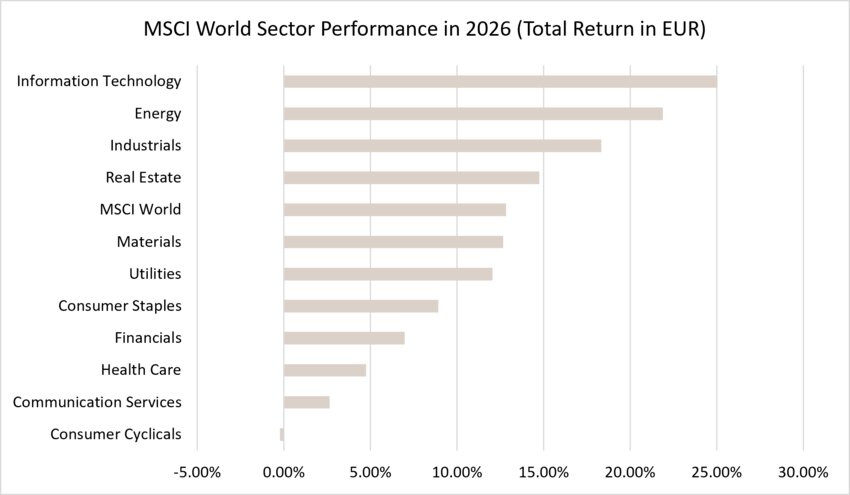

From a sector perspective, travel, insurance, healthcare and banking stocks were the most sought-after, while energy suffered from the decline in oil prices during the month. Technology stocks continued to be supported by AI momentum, although very strong recent performance has led to some profit-taking.

In the portfolios, profits were taken on emerging markets and Technology, following their strong growth. While the long-term outlook for AI remains favourable, a consolidation phase seems possible before the next earnings season. At the same time, exposure to Energy was increased, particularly in oil services companies, whose investment outlook is still strong under a scenario where oil prices are expected to remain higher than before the conflict. This allocation could be increased further in the event of a correction driven by geopolitical de-escalation. Finally, exposure to small and mid caps was increased to take advantage of the expected broadening of earnings growth, still-favourable macroeconomic conditions in the United States, and the potential for a rebound in valuations in Europe.

*Performances are calculated in euros

Sovereign yields and credit market

In June, central banks once again took centre stage, remaining highly attentive to the inflationary pressures caused by the conflict in the Middle East. Bond markets oscillated between fears of monetary tightening fuelled by more hawkish statements from the Fed and the ECB, and the easing allowed in the second half of the month, with oil prices down following the agreement reached between the United States and Iran.

Across the Atlantic, ongoing tensions in the Middle East, robust employment figures and an increasingly restrictive Fed initially pushed sovereign yields higher. Kevin Warsh's first meeting as Fed Chair made a lasting impression: although policy rates remained unchanged, the Fed's rhetoric revived expectations of a rate hike, pushing the 2-year US yield sharply higher. However, the easing of oil prices and slightly more favourable inflation figures in the second half of the month helped limit the rise in long-term yields: the US 10-year ended June at around 4,46%, down by around 3bp over the month.

In the eurozone, the ECB delivered its first rate hike since 2023 on 11 June, taking its deposit rate to 2,25%. While the decision was widely expected, Christine Lagarde maintained a firm tone, while suggesting that the pace of tightening could remain moderate. As in the United States, the fall in oil prices following the agreement with Iran subsequently supported a notable easing in inflation expectations. The 10-year Bund thus ended June at 2,85%, down 8bp over the month.

In the credit segment, movements remained limited. In the United States, Investment Grade spreads widened by 3bp to 76bp, while High Yield also widened by 3bp to 275bp. In the eurozone, spreads remained broadly stable, widening only slightly over the month. This reflects the resilience of credit despite the volatility linked to the Middle East conflict and the shift in tone from central banks.

Disclaimer

The recommendations contained in this document are, unless otherwise expressly stated, those of Spuerkeess Asset Management and are produced by Carlo Stronck, Managing Director & Conducting Officer, Aykut Efe, Economist & Strategist, Guillaume Gehant, Portfolio Manager and Martin Gallienne, Portfolio Manager, acting under an employment contract with Spuerkeess Asset Management.

Spuerkeess Asset Management is an entity supervised by the CSSF (Luxembourg’s financial sector supervisory authority) as a UCITS management company able to provide discretionary portfolio management and investment advisory services.

All external sources (financial information systems, Bloomberg and Refinitiv Datastream) are, unless expressly stated in the recommendation itself, deemed reliable, it being understood that Spuerkeess Asset Management cannot, however, fully guarantee the accuracy, completeness or relevance of the information used by these sources. The information may be either incomplete or condensed and cannot be used as the sole basis for valuing securities.

The valuation of financial instruments and issuers contained in this document is based on data provided by Bloomberg. The full description of the valuation method used by Bloomberg is available at www.bloomberg.com.

Any reference to past performances should not be construed as an indication of future performances. The price or value of the investments to which this document refers directly or indirectly may vary at any time against your interests. Any investment in financial instruments entails certain risks of which Spuerkeess (Banque et Caisse d’Épargne de l’État, Luxembourg) has been informed beforehand, such as the loss of the investment made.

With a view to providing these recommendations to Spuerkeess, Spuerkeess Asset Management has verified all relationships and circumstances that could reasonably be likely to undermine the objectivity of the recommendations contained in this document and confirms the absence of interests and conflicts of interest relating to any financial instrument or issuer to which the recommendations relate directly or indirectly, as well as those of the persons involved in producing these recommendations.

Recommendations are made on the date indicated on the first page of the document and were first released on the same date. The recommendations contained in this document may, where applicable, be used and therefore updated when Spuerkeess Asset Management next provides investment advice to Spuerkeess.

All recommendations sent by Spuerkeess Asset Management to Spuerkeess over the past twelve months may be consulted directly and free of charge at Spuerkeess Asset Management’s registered office, 19-21 rue Goethe, L-1637 Luxembourg. The information to be consulted shall include the date of dissemination of the recommendation concerned, the identity of the individual(s) involved in the production of the recommendation, the target price and the relevant market price at the time of dissemination, the direction of the recommendation concerned and the period of validity of the target price or recommendation.

The information contained in this document cannot be used as the sole basis for valuing securities and this document does not constitute an issue prospectus.

This document is for information purposes only and does not constitute an offer or solicitation to buy, sell or subscribe. Spuerkeess Asset Management may not be held liable for any consequences that may result from the use of any of the opinions or information contained in this document. The same is true for any omissions.

Spuerkeess Asset Management does not accept any liability for this document if it has been altered, distorted or falsified, particularly through online use.