A rebound is on the cards but won’t last forever

Investment Update - June 2025

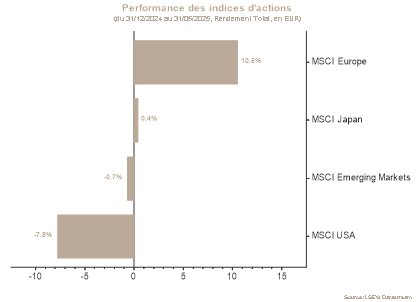

After a fairly complicated month of April, dragged down by US President Donald Trump’s announcements of “reciprocal tariffs”, the global equity markets rebounded in May. At the end of the month, the global index had gained nearly 6% in euros. Over the period, the US markets rose by 6,5%, Europe by 4,7%, and emerging indices by 4,3%.

Although the year got off to a difficult start, the announcement of a tariff pause restored investor confidence and brought the indices back to their pre-tariff war levels.

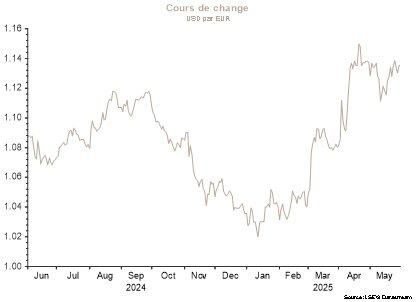

On the bond market, the trajectory of the 10-year reference rates trended upwards. In the United States, the 10-year sovereign rate rose from 4,16% to 4,4%: lurking in the background were fears about public debt sustainability and the new budget bill (the “One Big Beautiful Bill”), which launched the debate about potential tax cuts. In Germany, the 10-year rate ended the month slightly above its starting point, at 2,50%.

With the temporary suspension of tariffs and effective tariff rates now expected to be much lower than a month ago, the worst-case scenarios of recession and major stagflation were avoided.

But does this mean that this bout of volatility and companies’ reduced visibility will have no economic impact? There are no guarantees. While the equity indices have returned to pre-tariff announcement levels, the economic trajectory is not expected to emerge entirely unscathed.

Despite the announced pauses and cuts, effective tariff rates are ultimately expected to be three to four times higher than before Trump’s return to the White House. According to an independent study conducted by Yale University’s Budget Lab, the average US household is projected to lose nearly USD 2.800 in purchasing power compared with 2024 due to the higher inflation caused by implementation of the tariffs.

While it may be going too far to describe the future economic impacts as stagflation, the environment would on the whole be stagflationary, characterised by lower growth and higher inflation.

In Europe, in contrast, the European Central Bank (ECB) should be pleased that inflation is moving towards the 2% target, meaning it can maintain a downward bias on key interest rates. In addition to monetary support, Europe should also benefit from fiscal support as long as the new coalition in Berlin keeps its promises.

In this environment, a slight underweight to equities and a favourable bias towards the European markets over the US markets make more sense. The difficult economic trajectory, combined with a complacent market with high valuation levels, could lead to unpleasant surprises on the US markets. In sector terms, we continue to favour Communication Services, due mainly to its exposure to the artificial intelligence theme. We also like the European Real Estate sector to take advantage of European rate cuts.

From a bond perspective, we prefer European over US yields. In the United States, inflation expectations and public debt are making bonds less attractive, while in Europe they are likely to benefit from falling rates and subdued inflation. On the corporate debt side, we favour carry and quality through the investment-grade segment.

Stock markets

The equity market rebound continued in May, driven by improved household sentiment and easing trade tensions. Risk appetite made a strong comeback due in part to the delay in some of the tariff increases.

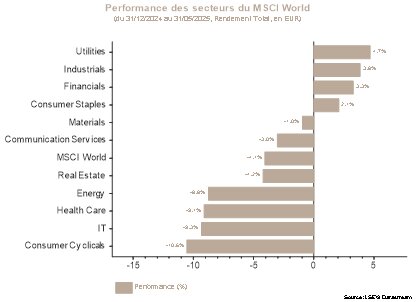

North American equities were the top performers, with the Technology and Consumer Discretionary sectors leading the way. Banking and industrial stocks dominated in Europe, while Healthcare lagged on both sides of the Atlantic.

North America and developed markets took the lead among major geographic regions, while China continued to underperform. It was held back by its still fragile economic and political context.

This environment prompted us to introduce an allocation targeted towards a basket of domestic European companies that are not highly dependent on global supply chains. It should be noted that these companies have the potential to outperform should trade tensions resurface.

Ultimately, a more acyclical positioning is called for at a time when valuations are high and macroeconomic balances remain uncertain.

Sovereign yields and the credit market

There was some turbulence on the interest rate markets in May. Government borrowing rates, in particular in the United States, cycled up and down under the effects of the political debates around tariffs and concerns about the outlook for US public finances.

In Germany, the interest rate on the 10-year government bond began the month at 2,44%, then rose as high as 2,70% at the height of the tensions before falling a bit to end the month at 2,50%. This slight final increase of 0,06% reflects investors’ clear understanding of US fiscal concerns, which are not expected to have a direct impact on the eurozone.

Rates moved even more in the United States: the 10-year bond initially stood at 4,16% before rising to 4,62% in mid-May and then ending the month at 4,40%.

The 30-year bond, which reflects very long-term confidence, spiked to 5,15% before coming back down to 4,93% at the end of the month.

This volatility was driven by concerns about the health of US public finances, after Moody’s downgraded the country’s credit rating, and to the heated debate around extending certain tax cuts.

The corporate debt markets were much more reassuring: the rates that businesses have to pay to borrow (the so-called spreads) have declined. Rates for healthy companies in the investment-grade category fell by 0,12% to end about 1% above government rates. The decline was even more pronounced (-0,40%) for riskier companies in the high-yield category, a sign that confidence has improved overall.

Lastly, Italy’s borrowing rates benefited from this positive climate, as the spread with Germany narrowed to 0,98%, its lowest level since September 2021.

All in all, and despite concerns about the US budget, investor confidence made a gradual comeback in May, with rates slightly higher on government bonds but a sharp easing on corporate debt.

Disclaimer

The recommendations contained in this document are, unless otherwise expressly stated, those of Spuerkeess Asset Management and are produced by Carlo Stronck, Managing Director & Conducting Officer, Aykut Efe, Economist & Strategist, Amina Touaibia, Portfolio Manager and Martin Gallienne, Portfolio Manager, acting under an employment contract with Spuerkeess Asset Management.

Spuerkeess Asset Management is an entity supervised by the CSSF (Luxembourg’s financial sector supervisory authority) as a UCITS management company able to provide discretionary portfolio management and investment advisory services.

All external sources (financial information systems, Bloomberg and Refinitiv Datastream) are, unless expressly stated in the recommendation itself, deemed reliable, it being understood that Spuerkeess Asset Management cannot, however, fully guarantee the accuracy, completeness or relevance of the information used by these sources. The information may be either incomplete or condensed and cannot be used as the sole basis for valuing securities.

The valuation of financial instruments and issuers contained in this document is based on data provided by Bloomberg. The full description of the valuation method used by Bloomberg is available at www.bloomberg.com.

Any reference to past performances should not be construed as an indication of future performances. The price or value of the investments to which this document refers directly or indirectly may vary at any time against your interests. Any investment in financial instruments entails certain risks of which Spuerkeess (Banque et Caisse d’Épargne de l’État, Luxembourg) has been informed beforehand, such as the loss of the investment made.

With a view to providing these recommendations to Spuerkeess, Spuerkeess Asset Management has verified all relationships and circumstances that could reasonably be likely to undermine the objectivity of the recommendations contained in this document and confirms the absence of interests and conflicts of interest relating to any financial instrument or issuer to which the recommendations relate directly or indirectly, as well as those of the persons involved in producing these recommendations.

Recommendations are made on the date indicated on the first page of the document and were first released on the same date. The recommendations contained in this document may, where applicable, be used and therefore updated when Spuerkeess Asset Management next provides investment advice to Spuerkeess.

All recommendations sent by Spuerkeess Asset Management to Spuerkeess over the past twelve months may be consulted directly and free of charge at Spuerkeess Asset Management’s registered office, 19-21 rue Goethe, L-1637 Luxembourg. The information to be consulted shall include the date of dissemination of the recommendation concerned, the identity of the individual(s) involved in the production of the recommendation, the target price and the relevant market price at the time of dissemination, the direction of the recommendation concerned and the period of validity of the target price or recommendation.

The information contained in this document cannot be used as the sole basis for valuing securities and this document does not constitute an issue prospectus.

This document is for information purposes only and does not constitute an offer or solicitation to buy, sell or subscribe. Spuerkeess Asset Management may not be held liable for any consequences that may result from the use of any of the opinions or information contained in this document. The same is true for any omissions.

Spuerkeess Asset Management does not accept any liability for this document if it has been altered, distorted or falsified, particularly through online use.