Even the fiercest winds eventually subside

Investment Update - April 2026

This March, showers went hand in hand with a return of volatility to the financial markets, triggering a fall of nearly 5%* in global equities following Israeli-American strikes on Iran.

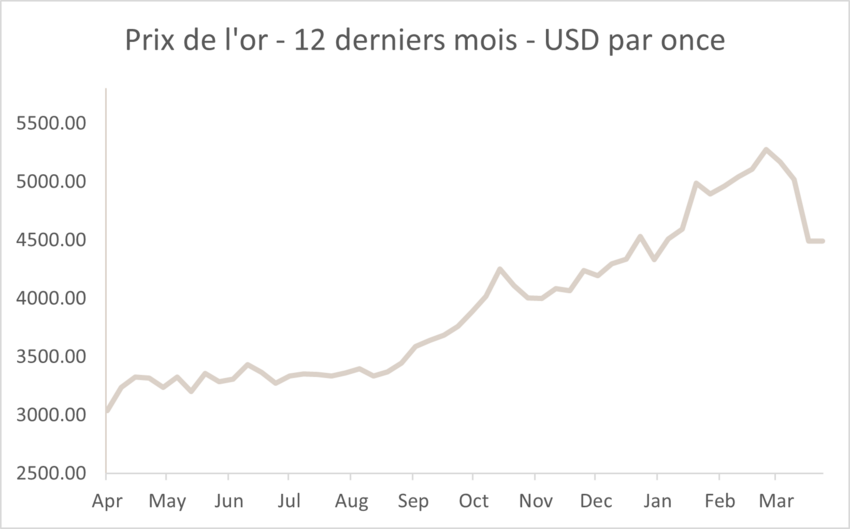

Volatility spared no asset class: oil rose by 63% in US dollars, gold fell by 11% and sovereign yields increased in both Europe and the United States.

The US 10-year yield rose from less than 4% to 4,32%. In Germany, the 10-year Bund followed suit, rising from 2,65% to more than 3%.

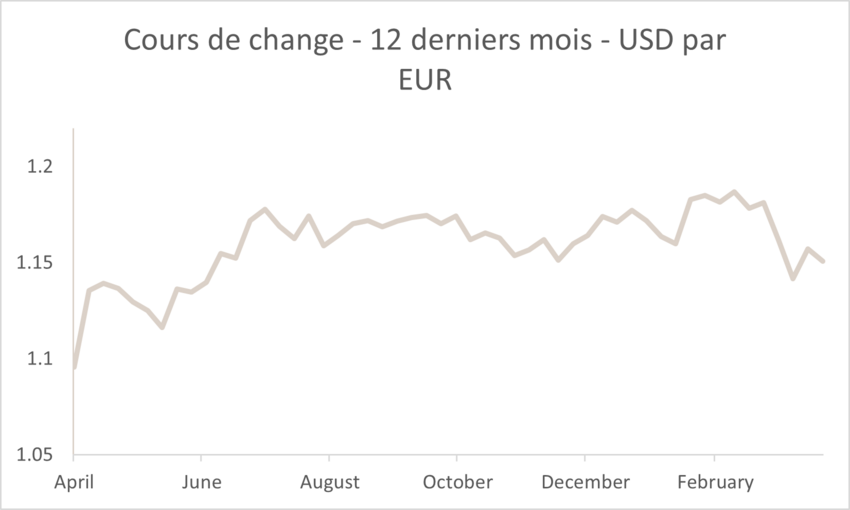

The dollar in particular acted as a safe haven, in a context where gold and bonds were unable to fulfil this role. As a result, European investors were able to offset more than 2% through exposure to the United States thanks to the dollar effect. Other regions, namely Europe, Japan and Emerging Markets, despite being the main winners during the first two months of the year, significantly underperformed in March, recording returns of -7,68%*, -10,25%* and -10,91%* respectively.

Armed conflicts gradually impacted oil and gas infrastructure, with the Strait of Hormuz at the centre of concerns, as 20% of global oil passes through it. At times, investors saw echoes of 2022: a rise in commodities generating fears of stagflation.

It goes without saying that the economic impact of the conflict will be closely tied to its duration and to disruptions in oil and gas production and transport. For example, Qatar rapidly halted production of liquefied natural gas (LNG), which accounts for nearly 20% of global output.

For now, the inflationary impact appears fairly certain in the short term. One-year inflation expectations are generally rising, but predictions that the conflict will be limited in duration have allowed longer-term expectations to remain moderate.

As a result, fears of stagflation have resurfaced. However, investors are not unanimous on this point.

With regard to central banks, expectations diverge. As inflationary pressures are stronger in Europe, bond markets are questioning whether the European Central Bank (ECB) could potentially raise its key rates one to two times in the coming months. In the United States, by contrast, a status quo on Federal Reserve (Fed) rates appears satisfactory.

For the moment, a high-inflation regime comparable to that of 2022 has been ruled out. Admittedly, the price of a barrel is soaring, but in 2022, in addition to the Ukrainian conflict, post-Covid bottlenecks and strong wage growth were already pushing inflation higher. Today, these same factors have eased considerably.

Against this backdrop, risk was reduced in portfolios through the sale of equities as soon as the conflict began. In addition, to take advantage of the diversifying role of the dollar and the United States’ position as an oil and gas producer, this region was significantly overweighted in portfolios at the expense of Europe and emerging markets, regions more vulnerable to the energy shock due to their dependence on imports.

From a sector perspective, Technology continues to offer significant growth opportunities with valuations that are very attractive compared with recent months. Other sectors such as Biotechnology, Banks and Consumer Discretionary continue to represent attractive investment themes.

Finally, on the bond segment, duration risk remains contained, with sovereign yields relatively unattractive in the United States but slightly more appealing in Europe. In credit, quality and carry remain favoured.

*Performances are calculated in euros.

Stock markets

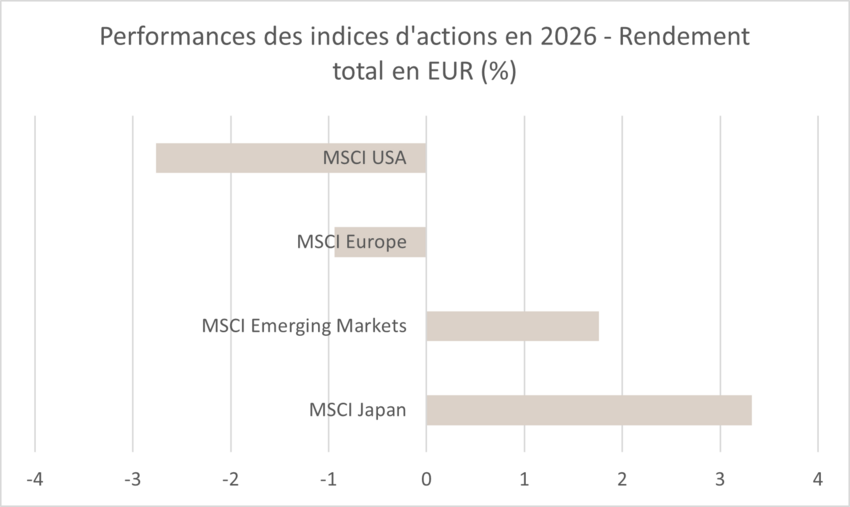

The outbreak of war in the Middle East at the beginning of the period created a highly unstable economic and geopolitical environment, leading to a rapid deterioration in global investor sentiment and a marked correction in major international indices. The escalation of tensions between the United States and Iran generated an energy shock of extreme magnitude, forcing investors to consider the possibility of stagflation. As a result, index performance was very negative: Emerging Markets fell by 9,4%* and the Japanese index by 8,6%*, followed closely by the MSCI China Index, down 4,5%*. Historically, in developed markets, this type of shock is seen as favourable to US markets and detrimental to European indices. This reading appears to be confirmed by the direction of the MSCI Europe in March, which fell by 8%* compared with MSCI North America at -4,76%*.

In fact, this strong underperformance reflects concerns about the spread of a growth shock, even though investors are clearly favouring the United States. The outperformance of US markets is notably explained, in theory, by lower exposure to the oil shock, as the country is a net exporter, whereas Europe is typically considered structurally dependent on energy flows from the Strait of Hormuz.

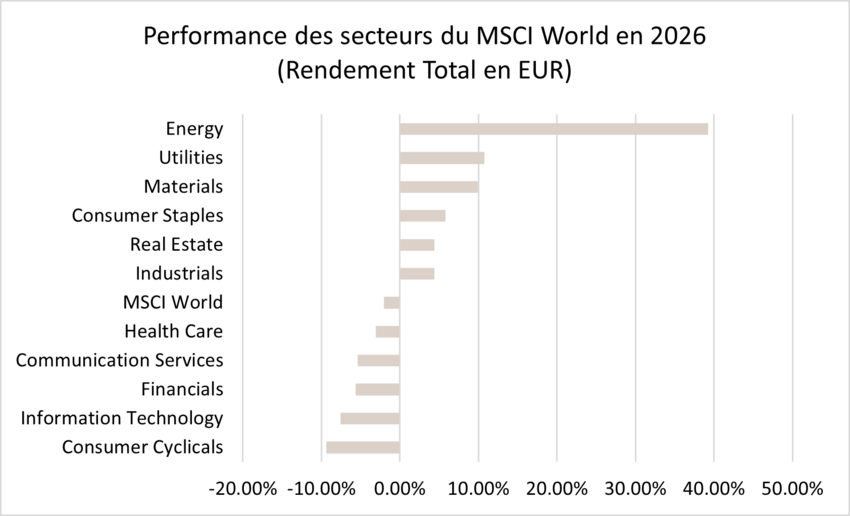

That said, with the exception of the Energy sector, which stood out significantly with a 15% increase in the MSCI ACWI Energy index, all other sectors ended the period in negative territory. However, risk premiums surged for the most cyclical segments and those most vulnerable to rising oil prices, in line with movements observed in Consumer Discretionary (-7,7%), Industrials (-9,5%) and Materials (-10%).

Sector allocation remained out of step with market trends: the overweight positions in Consumer Discretionary, Technology and Financials were maintained. In this context, it is important to note that Technology showed resilience by acting as a safe-haven sector given the long-term themes it encompasses. Although contrarian, this positioning is based on a pragmatic approach that incorporates the assumption of a significant rebound in the event of a gradual improvement in market visibility.

*Performances are calculated in euros

Sovereign yields and credit market

Bond markets alternated between sharp periods of tension and relief depending on announcements of a potential ceasefire. The monthly outcome following these intense fluctuations remains clearly negative.

In the US, Treasuries saw a sharp rise in yields. At the start of the month, the surge in oil prices, rising inflation expectations and several still-solid economic data points led markets to almost entirely price out the expected rate cuts from the Fed. In mid-March, the central bank left rates unchanged, but Jerome Powell adopted a more vigilant tone on inflation, emphasising the need for further progress before considering additional easing. Although some periods of easing appeared towards the end of the month amid diplomatic hopes and slightly less restrictive rhetoric, they were not enough to reverse the trend. The US 10-year yield ended at 4,32%, up 38 basis points (bps).

The eurozone experienced an even more pronounced movement, particularly on shorter maturities, as markets are more exposed to a lasting energy shock. Rising gas and oil prices, a rebound in core inflation and hawkish comments from several ECB members fuelled expectations of a possible resumption of rate hikes. Investors even moved to pricing in monetary tightening by the end of the year. Despite a partial decline at the very end of the period, the 10-year Bund closed the month at 3,00%, up 36 bps, marking its first return above this threshold since 2011.

On the credit segment, the month proved more resilient than the rise in macroeconomic volatility alone might have suggested. While spreads did widen, the magnitude was far more limited than the increase in risk-free rates. Investment Grade spreads widened by 13 bps to 95 bps in the euro area and by 5 bps to 89 bps in the United States. As a result, yields offered by credit increased significantly, with the average Investment Grade yield reaching 3,7%, representing attractive levels for long-term investors.

Disclaimer

The recommendations contained in this document are, unless otherwise expressly stated, those of Spuerkeess Asset Management and are produced by Carlo Stronck, Managing Director & Conducting Officer, Aykut Efe, Economist & Strategist, Amina Touaibia, Portfolio Manager and Martin Gallienne, Portfolio Manager, acting under an employment contract with Spuerkeess Asset Management.

Spuerkeess Asset Management is an entity supervised by the CSSF (Luxembourg’s financial sector supervisory authority) as a UCITS management company able to provide discretionary portfolio management and investment advisory services.

All external sources (financial information systems, Bloomberg and Refinitiv Datastream) are, unless expressly stated in the recommendation itself, deemed reliable, it being understood that Spuerkeess Asset Management cannot, however, fully guarantee the accuracy, completeness or relevance of the information used by these sources. The information may be either incomplete or condensed and cannot be used as the sole basis for valuing securities.

The valuation of financial instruments and issuers contained in this document is based on data provided by Bloomberg. The full description of the valuation method used by Bloomberg is available at www.bloomberg.com.

Any reference to past performances should not be construed as an indication of future performances. The price or value of the investments to which this document refers directly or indirectly may vary at any time against your interests. Any investment in financial instruments entails certain risks of which Spuerkeess (Banque et Caisse d’Épargne de l’État, Luxembourg) has been informed beforehand, such as the loss of the investment made.

With a view to providing these recommendations to Spuerkeess, Spuerkeess Asset Management has verified all relationships and circumstances that could reasonably be likely to undermine the objectivity of the recommendations contained in this document and confirms the absence of interests and conflicts of interest relating to any financial instrument or issuer to which the recommendations relate directly or indirectly, as well as those of the persons involved in producing these recommendations.

Recommendations are made on the date indicated on the first page of the document and were first released on the same date. The recommendations contained in this document may, where applicable, be used and therefore updated when Spuerkeess Asset Management next provides investment advice to Spuerkeess.

All recommendations sent by Spuerkeess Asset Management to Spuerkeess over the past twelve months may be consulted directly and free of charge at Spuerkeess Asset Management’s registered office, 19-21 rue Goethe, L-1637 Luxembourg. The information to be consulted shall include the date of dissemination of the recommendation concerned, the identity of the individual(s) involved in the production of the recommendation, the target price and the relevant market price at the time of dissemination, the direction of the recommendation concerned and the period of validity of the target price or recommendation.

The information contained in this document cannot be used as the sole basis for valuing securities and this document does not constitute an issue prospectus.

This document is for information purposes only and does not constitute an offer or solicitation to buy, sell or subscribe. Spuerkeess Asset Management may not be held liable for any consequences that may result from the use of any of the opinions or information contained in this document. The same is true for any omissions.

Spuerkeess Asset Management does not accept any liability for this document if it has been altered, distorted or falsified, particularly through online use.