A surprising reversal in sector performance

Investment Update - March 2026

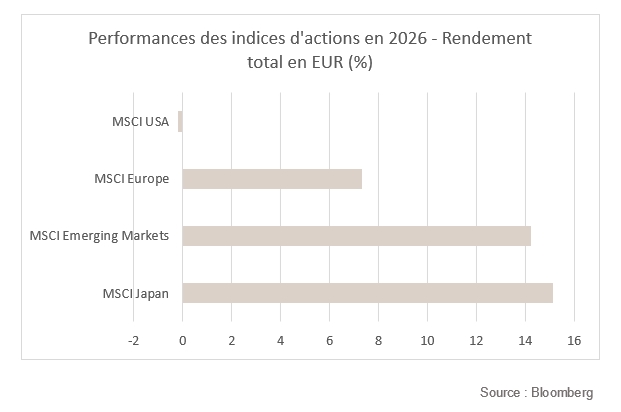

February was a good month for the equity markets, which gained 2,05%*, amid particularly strong geographical and sector rotation. While the US markets stagnated, Europe gained 4,1%*, emerging markets were up 7,4%* and Japan rose 9,3%*.

The rotation was not only geographical, it also affected style: small- and mid-cap stocks retained investors’ favour at the expense of US large caps, just as value stocks prevailed over growth.

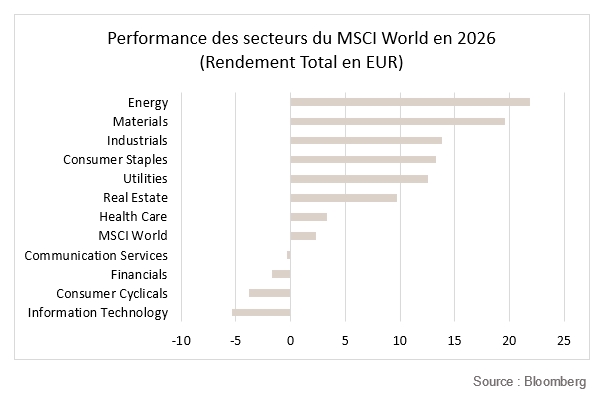

By sector, an unexpected group performed particularly well: cyclical sectors such as basic materials and energy led the way, followed by defensive sectors such as consumer staples and the service sector, which generally fare better during periods of economic contraction.

Technology and the artificial intelligence theme have been disregarded in recent weeks despite their very high performance in recent years. What explains this reversal? The latest advances in AI are worrying the sector as some of the new tools announced would significantly reduce dependence on certain tools or software.

Meanwhile, economic indicators were more positive. In the United States, although the decline in public spending weighed slightly on GDP in the fourth quarter (only 1,4% growth recorded), private consumption and business investment remain robust. Moreover, manufacturing indicators are increasingly encouraging, particularly new orders recorded in PMI readings.

As for inflation, while there are contrasting signs, it remains under control. According to various indicators, annual inflation is between 2,4% and 3% in the United States.

In this environment, sovereign rates were overall bearish. The US 10-year sovereign rate declined from 4,24% to 3,94%, and its German counterpart fell from 2,84% to 2,64%, against a backdrop of rising geopolitical fears ahead of the Israeli-US attacks on Iran.

As hostilities in the Middle East have returned to centre stage, oil prices have risen again, with spot prices close to $80 per barrel. This is a risky situation in terms of its ramifications for oil prices and the blockage of the Strait of Hormuz, and we reduced our equity allocation from overweight to neutral.

In geographical terms, the US has the advantage due to its gas and energy production, whereas Europe and Asia Pacific are both importers of oil and gas. In addition, the US continues to benefit from the strong dollar, which is currently enjoying its status as a safe-haven investment.

We are still underweight on bonds, with a short duration and a preference for corporate credit versus sovereign issues.

*Performances are calculated in euros.

Stock markets

There was strong regional divergence in February. Global equities rose slightly (+2,05%*) against a backdrop of increased volatility and a more risk-off mood at the end of the month. Asia-Pacific was the clear outperformer with the MSCI Asia Pacific index up +7,4%* over the month. Japan was particularly dynamic: the MSCI Japan index gained +9,3%*, supported by a wave of optimism after Sanae Takaichi’s election victory. In Europe, the market rose +4,1%* and reached a new all-time high mid-month, although some of its upside potential now seems priced in. In contrast, the US markets were more difficult to navigate. The MSCI North America was flat at -0,1%*, penalised by the consolidation of technology stocks and doubts on AI.

Sector dispersion was exceptional: the gap widened significantly, with nearly 15 points between the best and worst sector. Basic materials (+9,3%), utilities (+7,9%), energy (+7,8%) and consumer staples (+7,1%) benefited from rotation towards defensive segments in a more uncertain environment. In contrast, the telecoms (-5,5%), consumer discretionary (-4,6%) and technology (-4,9%) sectors suffered. In the background, doubts over AI dominated the markets, with questions as to the profitability of investments and the disruption of certain business models, while AI also sparked fears on private credit. Heightened risk aversion was also fuelled by inflation data, which rekindled concerns that rate cuts would be postponed, not to mention the rise in oil prices in a more tense geopolitical context (US-Iran), while trade uncertainties at the end of the month increased the risk premium on cyclical assets. In this context, we made no changes to our geographical and sectoral allocations. However, we made adjustments in consumer discretionary (increase in services) and banking stocks (geographical diversification with European stocks exposed to emerging countries).

*Performances are calculated in euros

Sovereign yields and credit market

The bond markets recorded a contrasting trend in February: despite solid US data and a more hawkish tone from the Fed, sovereign yields fell sharply under the combined effect of volatility on the equity markets and renewed geopolitical tensions. As a result, the markets gradually relegated macroeconomic fundamentals to the back burner in favour of a defensive repositioning.

In the US, the month started with resilient economic data while the Fed said it was in no hurry to ease monetary policy. However, the substantial correction of technology stocks, uncertainties about US trade and rising geopolitical risks in the Middle East revived demand for Treasuries. Despite generally resilient data, risk aversion dominated, leading to a significant easing of the curve. The 10-year rate ended the month at 3,94%, down 30 bp, while the 2-year rate dropped 15 bp to 3,37%.

In the eurozone, yields moved in line with Treasuries. After a tense start to the month at the long end due to budget debates and the past rise in Japanese yields, momentum reversed as the market climate became more cautious. Inflation showed signs of moderation in the eurozone, and the ECB maintained a balanced tone, with no sign of imminent change. Against this backdrop, the 10-year Bund closed the month at 2,64%, down 20 bp.

On the credit market, the situation deteriorated at the end of the period. Risk premiums widened – high yield by more than investment grade – in line with the equity volatility shock and the increase in risk aversion. Spreads widened by around +10 bp (US IG and EUR IG) and +30 bp (US HY and EUR HY) during the month. However, total returns were positive, driven by the easing of risk-free rates, and spreads are only marginally higher than they were at 31 December 2025.

Disclaimer

The recommendations contained in this document are, unless otherwise expressly stated, those of Spuerkeess Asset Management and are produced by Carlo Stronck, Managing Director & Conducting Officer, Aykut Efe, Economist & Strategist, Amina Touaibia, Portfolio Manager and Martin Gallienne, Portfolio Manager, acting under an employment contract with Spuerkeess Asset Management.

Spuerkeess Asset Management is an entity supervised by the CSSF (Luxembourg’s financial sector supervisory authority) as a UCITS management company able to provide discretionary portfolio management and investment advisory services.

All external sources (financial information systems, Bloomberg and Refinitiv Datastream) are, unless expressly stated in the recommendation itself, deemed reliable, it being understood that Spuerkeess Asset Management cannot, however, fully guarantee the accuracy, completeness or relevance of the information used by these sources. The information may be either incomplete or condensed and cannot be used as the sole basis for valuing securities.

The valuation of financial instruments and issuers contained in this document is based on data provided by Bloomberg. The full description of the valuation method used by Bloomberg is available at www.bloomberg.com.

Any reference to past performances should not be construed as an indication of future performances. The price or value of the investments to which this document refers directly or indirectly may vary at any time against your interests. Any investment in financial instruments entails certain risks of which Spuerkeess (Banque et Caisse d’Épargne de l’État, Luxembourg) has been informed beforehand, such as the loss of the investment made.

With a view to providing these recommendations to Spuerkeess, Spuerkeess Asset Management has verified all relationships and circumstances that could reasonably be likely to undermine the objectivity of the recommendations contained in this document and confirms the absence of interests and conflicts of interest relating to any financial instrument or issuer to which the recommendations relate directly or indirectly, as well as those of the persons involved in producing these recommendations.

Recommendations are made on the date indicated on the first page of the document and were first released on the same date. The recommendations contained in this document may, where applicable, be used and therefore updated when Spuerkeess Asset Management next provides investment advice to Spuerkeess.

All recommendations sent by Spuerkeess Asset Management to Spuerkeess over the past twelve months may be consulted directly and free of charge at Spuerkeess Asset Management’s registered office, 19-21 rue Goethe, L-1637 Luxembourg. The information to be consulted shall include the date of dissemination of the recommendation concerned, the identity of the individual(s) involved in the production of the recommendation, the target price and the relevant market price at the time of dissemination, the direction of the recommendation concerned and the period of validity of the target price or recommendation.

The information contained in this document cannot be used as the sole basis for valuing securities and this document does not constitute an issue prospectus.

This document is for information purposes only and does not constitute an offer or solicitation to buy, sell or subscribe. Spuerkeess Asset Management may not be held liable for any consequences that may result from the use of any of the opinions or information contained in this document. The same is true for any omissions.

Spuerkeess Asset Management does not accept any liability for this document if it has been altered, distorted or falsified, particularly through online use.